Global Computed Tomography Industry: Key Statistics and Insights in 2025-2033

Summary:

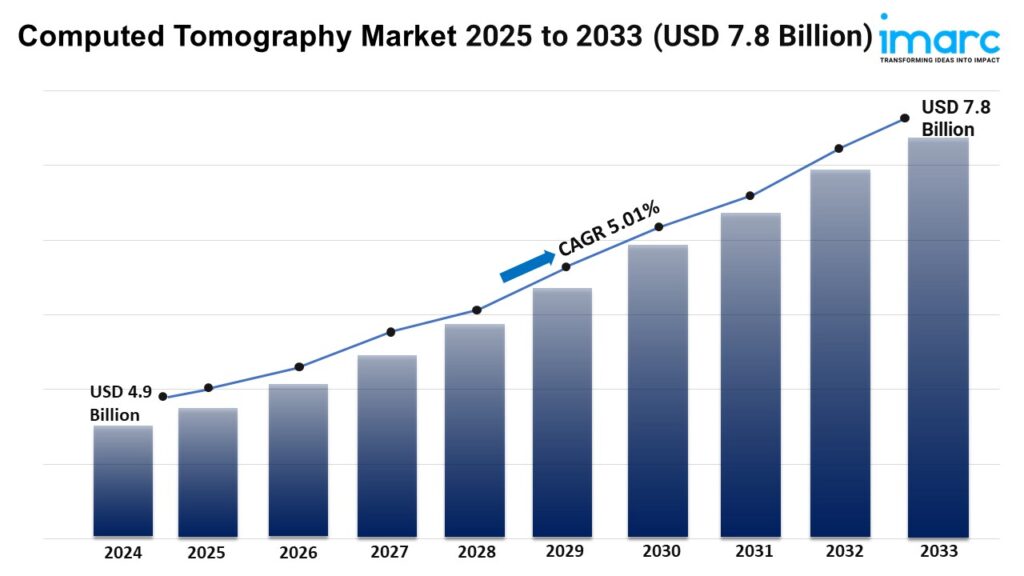

- The global computed tomography market size reached USD 4.9 Billion in 2024.

- The market is expected to reach USD 7.8 Billion by 2033, exhibiting a growth rate (CAGR) of 5.01% during 2025-2033.

- North America leads the market, accounting for the largest computed tomography market share.

- High slice accounts for the majority of the market share in the type segment due to their superior imaging capabilities.

- Oncology holds the largest share in the computed tomography industry.

- Hospitals remain a dominant segment in the market.

- The increasing incidence of chronic diseases like cancer, cardiovascular disorders, and respiratory conditions is a primary driver of the computed tomography market.

- Technological advancements in computed tomography (CT) systems are reshaping the computed tomography market.

Industry Trends and Drivers:

- Advancements in Imaging Technology:

Technological innovations are significantly propelling the market by improving imaging quality and diagnostic accuracy. The development of multi-slice computed tomography (CT) scanners allows for faster and more detailed image acquisition, enabling doctors to make more precise diagnoses. Moreover, innovations, such as dual-energy CT and spectral imaging, offer enhanced contrast differentiation, allowing for the identification of different tissues and abnormalities with greater clarity. These advancements are particularly important in fields, such as oncology, cardiology, and neurology, where detailed imaging is critical for disease detection and monitoring. Additionally, artificial intelligence (AI) integration in CT systems aids in automated image analysis, reducing human error and improving workflow efficiency in healthcare facilities. As these technologies continue to evolve, healthcare providers are upgrading their systems to stay competitive and meet the growing demand for high-quality diagnostic solutions.

- Rising Prevalence of Chronic Diseases:

The increasing incidence of chronic diseases like cancer, cardiovascular disorders, and respiratory conditions is a significant factor driving the demand for CT scans. Chronic conditions require ongoing diagnosis, monitoring, and treatment planning, all of which are facilitated by CT imaging. Moreover, CT scans are extensively used in oncology to detect tumors, evaluate the stage of cancer, and guide treatment approaches. In cardiology, CT angiography helps identify blockages or other issues in coronary arteries, providing critical information for heart disease management. The growing burden of these diseases, especially in aging populations and regions with high lifestyle-related illness rates, is leading to greater reliance on non-invasive diagnostic tools. The ability of CT scans to deliver quick and accurate results makes them indispensable in managing chronic diseases, thereby driving adoption and investment in CT technology across healthcare institutions globally.

- Increasing Geriatric Population:

The global rise in the elderly population is catalyzing the demand for CT scans. As people age, they become more susceptible to chronic illnesses, including cancer, cardiovascular diseases, and neurodegenerative conditions, which often require detailed imaging for accurate diagnosis and treatment planning. Older adults frequently undergo routine health assessments, and CT imaging plays a vital role in monitoring disease progression and the effectiveness of interventions. The higher frequency of age-related conditions, such as osteoporosis and stroke, increases the need for advanced imaging technologies to provide timely and accurate diagnoses. As healthcare systems globally prepare to handle the rising geriatric population, investments in medical imaging infrastructure, including CT scanners, are growing. This trend is driven by more healthcare providers incorporating advanced CT systems into their services to cater to the diagnostic needs of an aging society.

Request for a sample copy of this report: https://www.imarcgroup.com/computed-tomography-market/requestsample

Computed Tomography Market Report Segmentation:

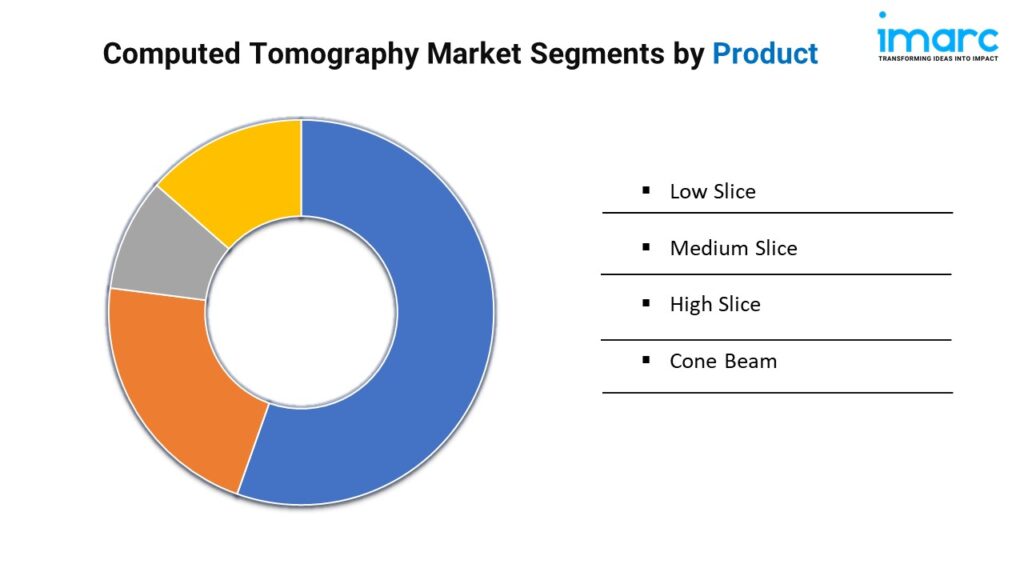

Breakup By Type:

- Low Slice

- Medium Slice

- High Slice

- Cone Beam

High slice represents the leading segment due to their superior imaging capabilities, faster scanning times, and ability to provide more detailed images for complex diagnoses.

Breakup By Application:

- Oncology

- Neurology

- Cardiovascular

- Musculoskeletal

- Others

Oncology accounts for the majority of the market share as CT scans are essential for detecting, staging, and monitoring various types of cancer, making them integral to cancer care.

Breakup By End User:

- Hospitals

- Diagnostic Centers

- Others

Hospitals hold the biggest market share because they are the primary healthcare facilities offering comprehensive diagnostic services, including advanced CT imaging.

Breakup By Region:

- North America (United States, Canada)

- Asia Pacific (China, Japan, India, South Korea, Australia, Indonesia, Others)

- Europe (Germany, France, United Kingdom, Italy, Spain, Russia, Others)

- Latin America (Brazil, Mexico, Others)

- Middle East and Africa

North America's dominance in the computed tomography market is owing to its well-established healthcare infrastructure, high healthcare spending, and the widespread adoption of advanced medical technologies.

Top Computed Tomography Market Leaders:

The computed tomography market research report outlines a detailed analysis of the competitive landscape, offering in-depth profiles of major companies. Some of the key players in the market are:

- Canon Medical Systems Corporation (Canon Inc.)

- FUJIFILM Holdings Corporation

- GE HealthCare (General Electric Company)

- Koning Corporation

- Koninklijke Philips N.V.

- NeuroLogica Corp. (Samsung Electronics Co. Ltd.)

- Neusoft Medical Systems Co. Ltd. (Neusoft Corporation)

- Planmeca Oy

- Siemens Healthineers AG (Siemens AG)

- Stryker Corporation

If you require any specific information that is not covered currently within the scope of the report, we will provide the same as a part of the customization.

About Us:

IMARC Group is a global management consulting firm that helps the world’s most ambitious changemakers to create a lasting impact. The company provide a comprehensive suite of market entry and expansion services. IMARC offerings include thorough market assessment, feasibility studies, company incorporation assistance, factory setup support, regulatory approvals and licensing navigation, branding, marketing and sales strategies, competitive landscape and benchmarking analyses, pricing and cost research, and procurement research.

Contact Us:

IMARC Group

134 N 4th St. Brooklyn, NY 11249, USA

Email: [email protected]

Tel No:(D) +91 120 433 0800

United States: +1-631-791-1145 | United Kingdom: +44-753-713-2163